Q3 2019 Outlook

Section 1: Q3 2019 Outlook

The Danger of Politicizing the Central Bank

As we enter the third quarter of 2019, we review recent global monetary policy and question how it has changed the traditional ways that we use it to detect risk in markets and the global economy.

The global economy is expected to continue to slow in the coming quarters resulting in lower inflation and downward pressure on interest rates. Central banks in developed and emerging markets are now generally cutting rates and quantitative easing (QE) is making a comeback. Weak economic data versus central bank activism remains the key theme.

Recently global markets have been encouraged by a truce in the trade war between the U.S. and China as President Trump and Chinese President Xi Jinping agreed to return to talks late in June. While the truce is encouraging following decades of growing trade flows and cooperation, the process of global trade integration faces risk of stalling or going in reverse. And while the U.S. has proven successful in securing a trade deal with Canada and Mexico (that has not yet been signed off on) and extracting some concessions from China, uncertainty remains due to the growing, rather than shrinking trade deficit in the U.S.

Trade contributed 0.94 percentage points to the U.S. economy’s 3.1% annualized growth pace in the first quarter. i Building on that trend, the U.S. trade deficit jumped to a five-month high in May, widening to USD 55.5 billion from a revised USD 51.2 billion in April. Imports surged 3.3% and exports rose 2%. The politically sensitive goods trade deficit with China increased 12.2% to USD 30.2 billion despite the recent increase in import tariffs on Chinese goods. Imports increased, likely as businesses restocked ahead of an increase in tariffs on Chinese merchandise. Data for April was also revised higher to show the trade gap widening to $51.2 billion instead of the previously reported $50.8 billion. ii

Many economists highlight that the most important role of the U.S. economy, as the largest economy in the world and the globally recognized main reserve currency, is in providing liquidity to the global economy and driving demand around the world. Contrary to current Trump trade policy, this implies that the U.S. trade deficit is central to global economic stability. The dollar’s role as the global reserve currency and primary tool for global transactions means that many other countries rely on holding dollar reserves, creating massive demand for U.S. financial assets. This means that the U.S. pays little for its foreign borrowing, allowing it to finance its high consumption at low cost, which boosts global demand.

The IMF Working Paper on Tariffs from May 2019 found that U.S. GDP would decline in scenarios that include retaliation on Chinese trade tariffs imposed by the U.S., but also that U.S. output would decline in the case where China only limits exports of selected goods to the United States. iii This is because those foreign goods (electronics and other manufacturing goods) are particularly difficult to substitute with domestic production, and thus tend to be replaced by additional imports from other countries.

The risk that the Trump trade standoff will unwittingly destabilize the entire global economy and thus have dire consequences for the U.S. economy itself is the greatest current risk to equity markets and the broader global economy.

Global Fundamentals and the Limits on Central Bank Action

After the June FOMC meeting Chair Powell signaled a strong easing bias but indicated a desire to learn more about upcoming policy and data developments. Since then the two main events – the G20 summit and June payrolls – have been positive. U.S. data show that growth has been solid for the first half of the year, supported by a strong labor market and strong financial markets. Inflation remains subdued, and inflation expectations have fallen such that they are no longer consistent with the Fed’s 2.0% target.

But the global picture has deteriorated, and business sentiment has fallen, suggesting that the outlook for the U.S. has also deteriorated. The ECB is expected to ease policy again as the euro area is heavily exposed to a further slowdown in global growth because it has much less policy flexibility. The shift in global policy bias toward easing has also affected the debate around likely Bank of Japan action too, prompted in part when Japanese government bond yields fell further into negative territory.

The gap that has opened between the U.S. manufacturing and non-manufacturing sectors makes clear that trade policy uncertainty is the primary driver of the slowdown. The case for an “insurance” ease remains strong as global growth momentum is slipping and the latest declines in U.S. and global business confidence have yet to be felt.

While it is understood that the unique position of the U.S. in the global economy warrants a central bank that considers the global economy, recent comments by President Trump suggest that his political motives for seeing a continuation of strong equity markets are an attempt to influence the central bank and Chair Powell. Trump’s call for rate cuts while reminding everyone that the American economy is the best it has ever been leads us to this conclusion and has distorted the ability of market participants to detect actual underlying risk.

Central banks in most modern economies are designed to be insulated from the short-term whims of politicians. The goal is to give central bankers the freedom to snuff out inflation, even if that hurts political leaders at election time. Since the global meltdown of 2008, central banks, in the name of protecting the economy, have reacted to sharp market falls by easing policy. Investors have been placated into seeing the stock market as a roller-coaster ride backed by engineers. This creates a false sense of confidence in those markets that can lead to larger negative shocks.

How long can bad news, by going to lower interest rates, be good news for equity prices? Signs that central banks have abandoned monetary policy normalization and are ready to provide additional policy stimulus have encouraged markets as we enter the third quarter of 2019.

Fed rate cuts may happen with the intent to reassure economic actors that the ongoing expansion will continue. But slowing economies and soft inflation imply lower revenue growth, excess capacity, and competitive pricing pressures. The risk is that monetary policy may delay the correction but not prevent it. Given the deterioration in the global economy and policy uncertainty at home, when the correction does come, it will be all the more unanticipated.

Market skepticism, asset purchase limitations, and the potential adverse effects of greater negative yields on banks are all issues we see challenging risk assets. We continue to hope that the U.S. will develop policies that jointly address the U.S.’s need for strong demand and full employment and the rest of the world’s need for dollars by channeling foreign capital into productive, job-creating domestic investment.

Section 2: 4 Themes

Theme 1: Slowing Global Growth

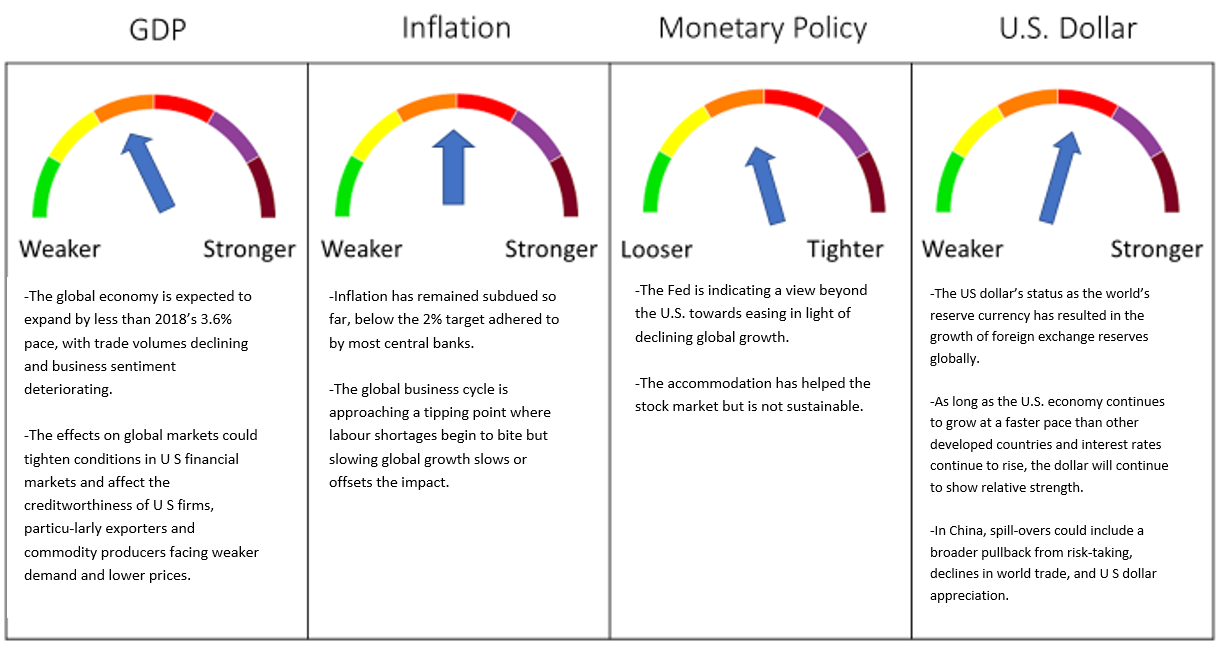

The pace of global growth is slowing this year as policy uncertainty takes its toll on the world’s economy. Data points to the global economy expanding by 3.3% this year, slower than 2018’s 3.6% pace, with trade volumes declining and business sentiment deteriorating. v

Economic and market risks are elevated as a result of the U.S. administration’s use of tariffs at a time when global growth is slowing. The prospect of a prolonged U.S.-China trade war, the lack of clarity around Brexit, and political and economic upheaval in countries like Venezuela have combined to generate downside risks to the outlook.

The stakes are high for this year’s European Parliamentary elections where the populists are likely to continue gaining ground, while lingering tensions and a lack of progress in Brexit negotiations raise the odds of a “hard Brexit” scenario. Another near-term risk, which was cited in the November FSR (Federal Reserve Financial Stability Report, May 2019) is elevated tensions between the European Commission and Italy over Italy’s budget plan, which had raised the country’s borrowing costs and prompted worries about its long-term fiscal sustainability. vi These concerns have been deferred for now, as Italy and the European Commission agreed on a budget plan for 2019, but Italy still faces longer-run fiscal challenges.

European economies have notable international financial and economic linkages, and a sharp economic downturn in Europe would affect banks, markets, and the global economy. Financial market volatility in Europe could spill over to global markets, including the United States, leading to a pullback of investors and financial institutions from riskier assets, which could amplify declines in equity prices and increases in credit spreads. In addition, spillover effects from banks in Europe could be transmitted to the U.S. financial system directly through credit exposures as well as indirectly through the common participation of globally active banks in a broad range of activities and markets. The consequent U.S. dollar appreciation and weaker global demand in such a scenario would depress the U.S. economy through trade channels, which could reduce earnings of some U.S. businesses, particularly exporters. Such effects could harm the creditworthiness of affected U.S. businesses, particularly those that already have high levels of debt.

Amid the uncertainty, global central banks have moved to the sidelines. Even with the economic expansion in its tenth year, contained inflation pressures have removed any urgency for central banks to act.

Theme 2: China’s Non-Financial Sector is Dangerously Over Leveraged

In China, the pace of economic growth has been slowing over the past several years, and a long period of rapid credit expansion has left the non-financial sector highly indebted and lenders more exposed in the event of a further slowdown.

Developments that significantly strain the repayment capacity of Chinese borrowers and financial intermediaries, including a further slowdown in growth or a collapse in Chinese real estate prices, could trigger a collapse in this market. If problems arise in China, spill¬overs could trigger a domino effect with a broader pullback from risk-taking, declines in world trade and commodity prices, and U.S. dollar appreciation resulting. Such an event would tighten conditions in U.S. financial markets and affect the creditworthiness of U.S. firms, particularly exporters and commodity producers facing weaker demand and lower prices. vii

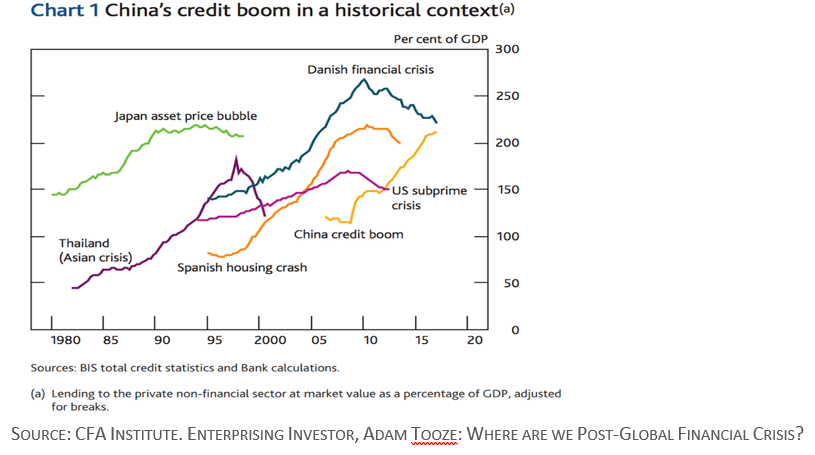

In the recently released book “Crash” by Adam Tooze, China’s credit boom is compared with other credit bubbles that ended badly. viii Tooze highlights that the U.K. banking sector has by far the heaviest exposure to Hong Kong and China in general — much more than the United States, Japan, or Europe. Although the Chinese have not slowed their credit bubble, they have shown an ability to restructure their banking sector in the past – in 1998 to 2005, for example – and more recently to shrink their shadow banking segment. The outlook for the global economy rides on how China manages its current credit situation. Trade-related uncertainty has made Chinese capex expansion less likely. On the monetary side, the ability to cut the reserve requirement ratio (RRR), or the benchmark interest rate and on the fiscal side, the government can issue more special local government bonds are both available. If the Chinese economy does stabilize this year, China’s currency could become a global currency stabilizer.

Theme 3: The U.S. Economy Balancing Act Between Slowing Manufacturing Growth and Strong Markets

The U.S. economy continued to grow at a solid clip in the first quarter of 2019 on the back of net exports and inventory building. ix Growth is likely to be somewhat weaker in Q2. Despite an uneven quarterly pattern, the key driver of the U.S. economy remains the consumer. Strong demand for labour pushed the unemployment rate to a 50-year low in early 2019 and wage growth accelerated. Non-farm employment increased by 224,000 jobs in June, handily beating expectations. The resilience of business hiring is in strong contrast to the recent business surveys’ generally downbeat message. In June, the unemployment rate edged up from 3.62% to 3.67%, and average hourly earnings increased only 0.2%. x

With more people working and wages rising faster than inflation, we expect consumer spending to increase this year. Business investment is also forecast to contribute to the economy as companies take advantage of last year’s cut in the corporate income tax rate and other supportive policies.

On trade policy, the U.S. is the instigator and the perpetuator. The recent removal of tariffs on steel and aluminum imports and the Trump Administration’s desire to ratify the new trade agreement with Canada and Mexico had dampened some of the pressures within North America. Unfortunately, the positive sentiment was crushed in late May when the U.S. threatened to levy tariffs on Mexican imports in order to force its southern neighbor to stem the flow of migrants. Tensions between the U.S. and China, meanwhile, have become increasingly heated after the U.S. bumped up tariff rates and made threats to expand the list of products affected.

The Fed can claim mission accomplished on getting the economy to full employment with most inflation measures at or slightly below the 2% target. Maintaining these conditions is the challenge now facing U.S. policymakers. The FOMC appears content to hold the fed funds rate at a slightly below neutral level as a nod to the risks to the economic outlook coming from an unpredictable presidency.

Theme 4: Canada Is Not an Island

Were Canada an island insulated from global developments, there would be little reason for concern about the economy. Growth is solid, the labor market is strong, and there is no sign of imbalances. But Canada is not an island, and global economic developments matter for its economy. With the global outlook having darkened in recent months, it is fair to say that downside risks prevail in Canada at this point, even if the domestic economy looks fine.

Falling oil prices and a deepening in the housing-market correction saw Canada’s economy grow at just a 0.3% annualized rate in the last quarter of 2018 and contributed to the economy growing at a similar pace in the first quarter of this year. xi A recovery in oil production, easing of pressure in the housing market and the end of an unseasonably cold winter saw the economy post a solid increase in March, paving the way for stronger gains ahead.

Canada’s own tensions with the U.S. have eased with the removal of U.S. steel and aluminum tariffs along with Canadian retaliatory measures. But the ongoing close integration of cross-border production chains means that anything that hurts the U.S. industrial sector will have spillovers to Canada. Concerns about a slowing in global growth could also spill over to Canada’s resource-producing regions via lower commodity prices.

Canadian business confidence has weakened with the manufacturing sentiment index slipping into negative territory in April for the first time in more than three years. xii Global policy uncertainty, frictions with the U.S., and the Chinese government’s banning of Canadian canola all played into the decline.

Although the recent removal of tariffs on steel and aluminum by both the Canadian and U.S. governments and renewed efforts to ratify the updated NAFTA set up to restore confidence, the impact will be limited by the persistence of tensions between the U.S., China, Europe, and Mexico, Canada’s top trading partners. We view the Bank of Canada as more likely to cut rates later this year than not, but we expect those cuts to arrive after the Fed cuts. The difference in timing and magnitude may give the Canadian dollar a slight upward bias relative to its southern neighbor but likely not a large enough one to pose economic danger.

Should significant problems arise in China, spill¬over effects could include a broader pullback from risk-taking, declines in world trade and commodity prices, and U.S. dollar appreciation. The effects on global markets could be exacerbated if they deepen the stresses in already vulnerable EMEs. These dynamics could tighten conditions in U.S. financial markets and affect the creditworthiness of U.S. firms, particularly exporters and commodity producers facing weaker demand and lower prices.

Section 3. Investment Outlook

Slowing Global Growth While the U.S. Fed Pulls Back on Tightening Leads Us to a Stagnation Forecast for the Next Twelve Months

SOURCE: FRAME GLOBAL ASSET MANAGEMENT

Frame Global Asset Management considers these trends and factors them into our outlook for the economy in our twelve-month forward period. We look back to periods of similar economic behavior and use this information to predict the future behavior of the asset classes that we consider. Our investment process allows us to adapt for non-traditional monetary policy and other exogenous variables.

Section 4. June 2019 Portfolio Models

Our outlook is focused on tension between politics, policy, and the positioning of the corporate sector. The world economy remains vulnerable to the U.S-China power play. If tariffs persist or are ramped up further, already-weak world trade volumes will struggle to gain traction. In addition, rising political conflict (Brexit and Italy) and uncertainty have weighed on business sentiment over the past year and global capex is stalling. The dovish stance by central banks supports our Stagnation outlook for the U.S. economy as growth is capped over our forecast time horizon of twelve months.

China is committed to maintaining 6% growth and will respond to any slowing with further easing. xiii The U.S. and China have each raised tariffs and appear to be broadening the conflict to their respective tech sectors. The results of the European Parliament elections showed a significant step up in support for populist parties, who now control 28% of total seats in Parliament, up from 22% before. Turnout in the elections was low at 37%, some 30%-35% lower than may be expected in a general election or second referendum. xiv The Brexit Party’s win (mostly at the expense of the Conservatives) sent the message that many voters are willing to support a no-deal.

We will continue to monitor the data for growth, inflation, and recession signals from employment, consumer spending, business sentiment, Fed policy, the yield curve, inflation, and global economics. Our focus is on protecting portfolios from downside risk, and we believe that our investment process is working to achieve that goal.

Deborah Frame, CFA, MBA

President and Chief Investment Officer

July 14, 2019

iTrading Economics, U.S. Balance of Trade. July 3, 2019.

iiTrading Economics, U.S. Balance of Trade. July 3, 2019.

iiiCaceres, C., and Cerdeiro, D. A., 2019. IMF Working Paper. Strategy, Policy, and Review Department and Western Hemisphere Department. Trade Wars and Trade Deals: Estimated Effects using a Multi-Sector Model.

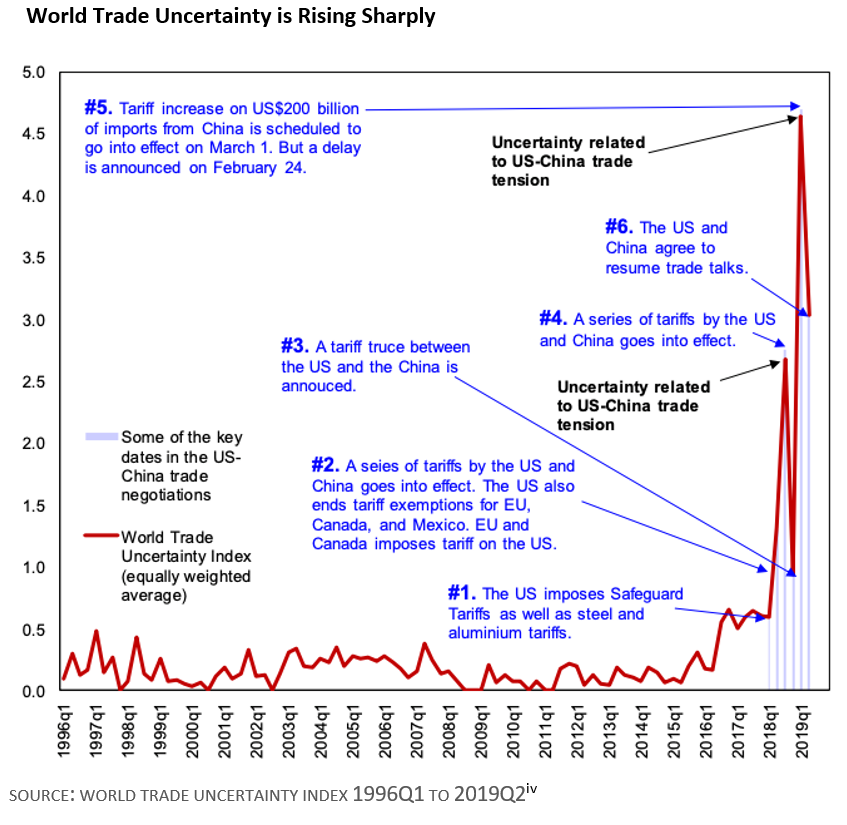

ivAhir, H., Bloom, N., Furceri, D. Caution: Trade uncertainty is rising and can harm the global economy. 4 July 2019. The source for the data on key dates in the U.S.-China trade negotiations comes from Bown and Kolb (2019). Item #6 comes from the BBC (2019). Note 1: The font in blue indicates the tariff measure taken, and the font in black indicates the narrative of the World Trade Uncertainty index. The WTU index is computed by counting the frequency of uncertain (or the variant) that are near the following words: protectionism, North American Free Trade Agreement (NAFTA), tariff, trade, United Nations Conference on Trade and Development (UNCTAD) and World Trade Organization (WTO) in EIU country reports. The WUI is then normalized by total number of words and rescaled by multiplying by 100,000. A higher number means higher trade uncertainty and vice versa. Note 2: The WUI is computed by counting the frequency of uncertain (or the variant) in Economist Intelligence Unit country reports. The WUI is then normalized by total number of words and rescaled by multiplying by 1,000. The WUI is then normalized by total number of words, rescaled by multiplying by 1,000, and using the average of 1996Q1 to 2010Q4 such that 1996Q1-2010Q4 = 100. A higher number means higher uncertainty and vice versa. While the latest spike is the result of uncertainty over Brexit and US trade policy, trade uncertainty explains more than 70% of the increase in uncertainty since the first quarter of 2018.

vIMF. World Economic Outlook. Growth Slowdown, Precarious Recovery. April 2019.

viFederal Reserve Financial Stability Report. Near-Term Risks to the Financial System. May 2019.

viiFederal Reserve Financial Stability Report. Near-Term Risks to the Financial System. May 2019.

viiiTooze, A., “Health of the Global Banking Sector: Differences by Region.” Columbia University.

ixTrading Economics, U.S. GDP. June 27, 2019.

xBureau of Labor Statistics. Economic News Release. Employment Situation Summary. July 5, 2019.

xiTrading Economics, Canada GDP. July 11, 2019.

xiiTrading Economics, Canada GDP. July 11, 2019.

xiiiSouth China Morning Post. China lowers 2019 GDP growth target to 6-6.5 per cent range. March 5, 2019.

xivJ.P. Morgan Economic Research. Global Data Watch. May 31, 2019.