Q1 2019 Outlook

Section 1. Q1 2019 Outlook

As we enter 2019, there is a heightened focus on downside risks both domestically and globally in the markets and in the broader economy. A negative feedback loop has emerged that is centered in the U.S., linking bad policy choices to falling asset prices, tighter financial conditions, and weaker corporate earnings.

The IMF said in an update to its World Economic Outlook in October that it is now predicting 3.7% global growth in both 2018 and 2019, down from its July forecast of 3.9% growth for both years. i

Across emerging market and developing economies, prospects are mixed. The downgrade reflects several factors, including the introduction of import tariffs between the United States and China, weaker performances by eurozone countries, and rising interest rates that are pressuring some emerging markets with capital outflows into the stronger U.S. dollar, notably Argentina, Brazil, Turkey, South Africa, Indonesia, and Mexico. Forward projections are less good for Latin America, the Middle East, sub-Saharan Africa, and Iran, reflecting the impact of the reinstatement of US sanctions. ii

In conjunction with the global growth downgrade, the IMF downgraded the 2019 U.S. growth forecast to 2.5% from 2.7% and cut China’s 2019 growth forecast to 6.2% from 6.4%. iii

Since the October IMF Report, tighter monetary conditions and the intensification of trade tensions have had a further impact on business and financial market sentiment, triggering financial market volatility and slowing investment and trade.

U.S. Policy Reversal Required

The U.S. move to more restrictive monetary policy includes both increasing the fed funds rate and removing liquidity across markets as Quantitative Easing is unwound by not rolling over treasury bonds on the federal balance sheet as they mature. This has led to greater tightening than the rising of the fed funds rate alone would cause. The combination has led to market volatility rising from the greater sensitivity to the price impact of minor macroeconomic events.

SOURCE: BANK FOR INTERNATIONAL SETTLEMENTS, FACTSET, J.P. MORGAN ASSET MANAGEMENT.

DATA AS OF NOVEMBER 8, 2018.

Emerging markets have been impacted particularly hard by U.S fiscal stimulus and monetary policy tightening. As a result, emerging economies have experienced capital flight and rising dollar-denominated debt. The ongoing threat of higher trade barriers that would disrupt global supply chains and slow the spread of new technologies, ultimately lowering global productivity, would feed into higher volatility. These restrictions would also make consumer goods less affordable, harming low-income households disproportionately.

Those relying heavily on exports have suffered the effects of lower commodity prices, and those trading indirectly with China have also felt the effects of the trade war. The deflationary effects of global recession are expected to erode inflation and increase global demand for high quality cash and fixed income, which would most certainly find its way to the United States.

SOURCE: VANGUARD RESEARCH. DECEMBER 2018.

VANGUARD CALCULATIONS BASED ON FEDERAL RESERVE’S FRB/US MODEL.

The threat of a global recession is real, as the U.S. is the largest global economy and the US Dollar remains the world’s reserve currency. While trade wars would create long-term negative impacts to the global economy, the U.S. “America First” policy has pushed up short-and long-term interest rates and strengthened the dollar relative to other currencies.

The problem is not that trade practices in the rest of the world are creating the U.S. trade deficit, rather that the economic policies of the United States are the source of the problem. US Dollar strength will continue to make the trade imbalance wider, giving protectionists more ammunition to raise the ante in a spiraling situation.

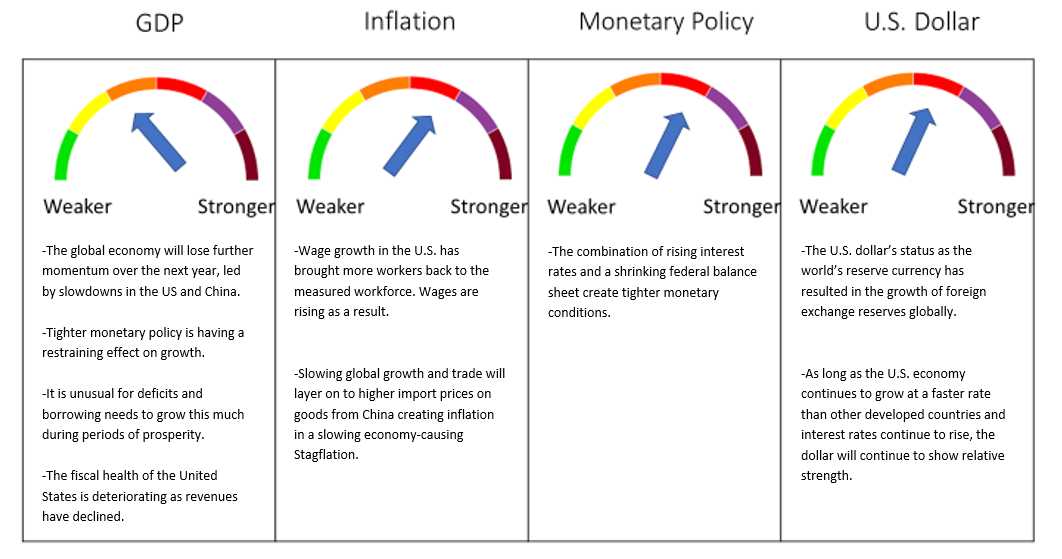

Our concern is that current policies are expected to have stagflationary effects (reduced growth alongside higher inflation). A limit in foreign direct investment and broad restrictions on immigration, which reduce labor-supply growth at a time when workforce aging and skills mismatch, would continue to contribute to the problem.

To break the loop, three policy reversals must happen. The first is to reign in massive U.S. deficit spending that is occurring during a period of economic expansion. The second is that monetary policy, including rising interest rates and a shrinking fed balance sheet, needs to be slowed or reversed. And third, a truce on U.S.-China trade must hold beyond March.

Until we see these policy reversals, our Outlook for the next twelve-month period is for six months of Stagnation followed by six months of Recession.

Meanwhile in Canada

The Canadian economy is set to weather the current slump in global oil prices better than it did in 2015, but we expect it will not escape unscathed. The 9,300 job increase in employment in December was better than expected, and the unemployment rate held at a 40-year low of 5.6%. iv The housing market is showing signs of weakness, and there are signs that higher interest rates are starting to weigh on consumer spending. v In the absence of further rate hikes, we expect GDP growth to slow from 2.0% in 2018 to 1.5% in 2019. The Bank will likely cut rates in 2019.

Frame Global Asset Management adheres to an investment process that focuses first and foremost on identifying and minimizing downside risk. We do this by recognizing the past relationships between asset class behavior in economic environments and analyzing the current environment and relationship with asset classes.

Section 2. Four Themes

Theme 1: Less Liquidity in U.S. Financial Markets

Recessions are typically triggered by policy mistakes, and the Federal Reserve may very well be on the road to making one as fears that the central bank will raise interest rates by too much and too quickly weighed heavily on stocks in 2018.

The Fed increased its target rate four times in 2018, with the final hike of the year coming in December, sending the equity markets into a tailspin. vi The Federal Open Market Committee (FOMC) implements monetary policy to help maintain an inflation rate of 2% over the medium term. The FOMC judges that inflation at the rate of 2% (as measured by the annual change in the price index for personal consumption expenditures, or PCE) is most consistent over the long run with the Federal Reserve’s mandate for price stability and maximum employment.

The policy statement that accompanied the Fed’s latest rate hike did attempt to allay fears that the Fed would tighten too much by acknowledging the economic outlook has diminished and that the balance of risks was now roughly even. FOMC participants also slightly lowered their expectations for the federal funds rate and now call for just two rate hikes in 2019 and one more after that. The drawdown of the Fed’s balance sheet is expected to run off at about $6 billion a month and mortgage-backed securities to run off at about $4 billion a month, rising to a combined maximum $50 billion a month in 2019. vii

While this ongoing move to tighten monetary conditions was underway throughout 2018, fiscal policy via massive tax reform changes was intended to provide stimulus to the already robust U.S. economy. 2018 kicked off with the enactment of tax cuts that pushed up long-term interest rates and created a sugar high in an economy that was close to full employment.

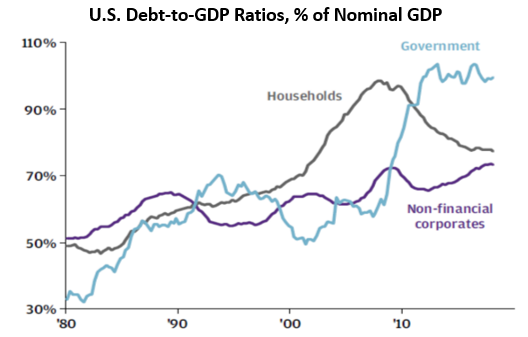

Supporters of the tax cuts repeatedly claimed the bill would increase economic growth enough to offset the decline in tax receipts, but corporate tax revenues are down one-third from a year ago. Total federal revenues ran $200 billion behind the Congressional Budget Office’s forecast for the 2018 fiscal year even while economic growth was faster than the C.B.O. expected. The nonpartisan Committee for a Responsible Federal Budget reports that nominal federal revenues are down by at least 3.6% since the tax cuts took effect. The federal budget deficit — the gap between what the government collects in revenues and what it spends — rose to $779 billion in the 2018 fiscal year ending September 30, a 17% increase from the prior year. viii

The continuing growth in the budget gap means the Treasury must borrow more to keep the government running. A total of $1.338 trillion is expected to be borrowed from global investors this calendar year, 145% higher than the $546 billion borrowed last year. This would be the highest level of borrowing since 2010, back when the American economy was struggling to recover from the Great Recession. ix

One of the consequences of the tax code changes was that in the first half of 2018, about $270 billion in corporate profits previously held overseas were repatriated to the United States and spent. Some 46% of that amount was spent on $124 billion in stock buybacks. x

The flow of repatriated corporate cash is just one example of the flood of payouts to shareholders, both as buybacks and dividends. Such payouts are expected to rise by 28% this year to almost $1.3 trillion. The surge in buybacks has added controversy over the tax cut package that President Trump championed. Republicans said the deal would be “rocket fuel” for the American economy. Democrats argued the share buybacks show that the tax cuts were a giveaway to the wealthy and won’t stimulate corporate investments and job creation.

It’s highly unusual for deficits and borrowing needs to grow this much during periods of prosperity. Despite a strong economy, the fiscal health of the United States is deteriorating fast, as revenues have declined.

Theme 2: Rising Global Trade Restrictions

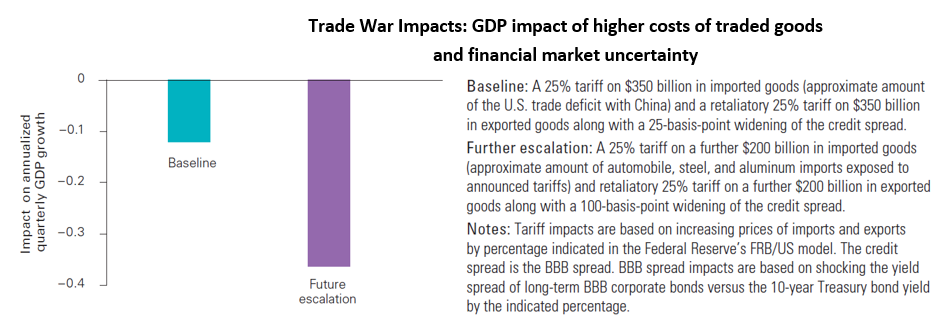

Escalating trade tensions and the potential shift away from a multilateral, rules-based trading system are key threats to the global outlook. An intensification of trade tensions and the associated rise in policy uncertainty has already triggered financial market volatility and slowed investment and trade. The latest U.S. actions against China seem to fuel a broader trade, economic, and geopolitical cold war.

Since the IMF’s April 2018 World Economic Outlook, protectionist rhetoric has increasingly turned into action, with the United States imposing tariffs on a variety of imports.

Following tariff increases in early 2018 on washing machines, solar cells, steel, and aluminum, the United States announced a 25% tariff on June 15th on imports from China worth $50 billion; China announced retaliation on a similar scale. On September 17th, the United States announced a 10% tariff—rising to 25% by year end—on an additional $200 billion in imports from China. In response, China announced tariffs on a further $60 billion of U.S. imports. The United States has also suggested that a further $267 billion of Chinese goods—covering nearly all remaining Chinese imports—may be hit with tariffs, and it has separately raised the possibility of tariffs on the automotive sector that would affect many other countries. xi

The two countries’ trade teams have been given until March 1st to agree on structural changes in China with respect to “forced technology transfer, intellectual property protection, non-tariff barriers, cyber intrusions and cyber theft, services, and agriculture”. American authorities have long accused China’s government of forcing foreign companies to give their proprietary technology to Chinese partners, but such demands are not enshrined in Chinese legislation and not recorded.

Permanently higher trade barriers would disrupt global supply chains and slow the spread of new technologies, ultimately lowering global productivity and welfare. Restrictions would also make tradable consumer goods less affordable, harming low-income households disproportionately.

Theme 3: Slowing Global Growth

The surge in the U.S. ADP measure of private employment to 271,000 jobs in December provides further evidence that, for all the recent volatility in financial markets, the U.S. economy is in healthy shape going into 2019. xii It appears that higher wages are the reason why people are returning to the active labour force in large numbers. Average hourly earnings increased by 0.4% m/m last month, enough to push the annual growth rate up to a near-decade high of 3.2%, from 3.1%. xiii

However, tightening monetary policy, worsening economic disputes, and slower demand from China are three key drivers that will dominate a weaker growth outlook in 2019.

Like U.S. equities, Chinese equities struggled in 2018 amid continued trade tensions and uncertainty over the health of the Chinese economy. Trade talks are likely to remain a major focal point in 2019, especially after news that China’s manufacturing sector contracted in December for the first time in 19 months. The S&P China 500 completed 2018 with a loss of 19%. xiv

Elsewhere, the risk of the UK withdrawing from the EU without a trade agreement in place has risen, while domestic political risks will likely continue to weigh on the credit outlooks for Italy, Brazil, Turkey, and Argentina.

Global credit conditions are expected to weaken in 2019 as economic growth decelerates, funding costs increase, liquidity tightens, and market volatility returns. Trade, political and geopolitical risks will likely escalate as tensions between the U.S. and China heighten. In addition, consequences of slower growth will increasingly thrust globalization and inequality debates into the political arena.

Theme 4: The Return of Market Volatility – More Expected in 2019

Volatility has made a comeback in recent months as a litany of concerns from U.S. policy to China-U.S. trade to tightening financial conditions to slowing earnings growth have overwhelmed investors, leading to broad-based, short-term panic selling.

Both monthly index volatility and average constituent correlations for the S&P 500 reached a five-year high, due to higher trading volumes in U.S. equities coupled with December’s decline in liquidity. xv Dispersion among U.S. equities declined during December, with earnings reports largely completed and broader themes dominating sentiment.

In 2018, the S&P 500 exhibited higher volatility, higher correlations, and higher dispersion compared with 2017, with monthly correlations and volatility averaging more than double last year’s levels. In December, the one-month volatility of the S&P 500 spiked to its highest level since 2012, surpassing previous highs in February 2018 and August 2015. xvi More than 40% of trading days in December saw the S&P 500 fall over 1%, triple the historical average. xvii The loss of 2.7% on December 24 for the S&P 500 was the largest percentage decline on the trading day before Christmas ever. This was followed by a 5% gain on December 26, which represented the largest percentage gain since March 23, 2009. xviii It is worth noting that volatility is still nowhere near the levels seen during the heights of the financial crisis.

Section 3. Investment Outlook

Slowing U.S. Growth in the first half of the year, with rising inflation leading to a Recession in the back half of the year

SOURCE: FRAME GLOBAL ASSET MANAGEMENT

Frame Global Asset Management considers these trends and factors them into our outlook for the economy in our twelve-month forward period. We look back to periods of similar economic behavior and use this information to predict the future behavior of the asset classes that we consider. Our investment process allows us to adapt for non-traditional monetary policy and other exogenous variables.

Section 4. December 2018 Portfolio Models

In December, we revised our twelve-month forward outlook to reflect the current counterbalancing influences of inflation on the U.S. economy. We believe that the U.S. is moving toward an inflationary environment that will occur just as growth is slowing. The December Outlook factored in six months of growth followed by six months of inflation over the twelve-month forecast period.

Recent reasons to hope for a more stable global economy in 2019 are contending with reasons to worry. Hope has come from the temporary US-China tariff truce and an oil supply shock that will positively impact global consumer spending next quarter. Concern remains as global geopolitical risks escalate, and the fading benefit of fiscal stimulus combined with tighter monetary policy in the U.S. causes a slowdown in rate-sensitive sectors that will likely spread to the broader economy and beyond the U.S. borders if not addressed. Global business surveys indicate declines in activity in China and softness in most European countries.

In December, we continued to maintain our current asset allocation across all models. This asset allocation is reflective of the current relative attractiveness of interest rates in the U.S. versus the rest of the world.

Deborah Frame, CFA, MBA

President and Chief Investment Officer

January 14, 2019

iInternational Monetary Fund, World Economic Outlook. October 2018.

iiInternational Monetary Fund, World Economic Outlook. October 2018.

iiiInternational Monetary Fund, World Economic Outlook. October 2018.

ivTrading Economics, Canadian Employment. December 2018.

vTrading Economics, Canadian Housing Market. December 2018.

viFederal Open Market Committee Transcripts. 2018.

viiFederal Open Market Committee Transcripts. 2018.

viiiCBO. Monthly Budget Review: Summary for Fiscal Year 2018.

ixCBO. Monthly Budget Review: Summary for Fiscal Year 2018.

xTankersley, Jim & Phillips, Matt. 2018. Trump’s Tax Cut Was Supposed to Change Corporate Behavior. Here’s What Happened. New York Times. November 12.

xiInternational Monetary Fund, World Economic Outlook. October 2018.

xiiADP National Employment Report. January 3, 2019.

xiiiBMO Capital Markets Economics Focus. January 4, 2019.

xivS&P Dow Jones Indices. Index Dashboard: Asia. December 31, 2018.

xvS&P Dow Jones Dashboard, Dispersion, Volatility, and Correlation. December 31, 2018.

xviBMO Capital Markets. US Strategy Snapshot. January 2, 2019.

xviiBMO Capital Markets. US Strategy Snapshot. January 2, 2019.

xviiiBMO Capital Markets. US Strategy Snapshot. January 2, 2019.